Silicon Carbide (SiC) Wafer (6-inch, 8-inch) Market, Trends, Business Strategies 2026-2034

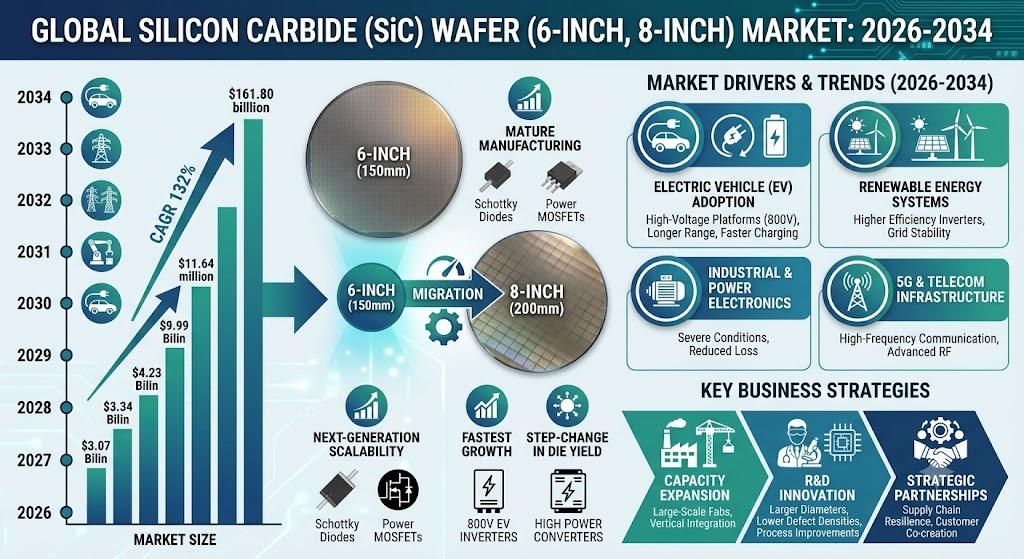

The global Silicon Carbide (SiC) Wafer (6‑inch, 8‑inch) Market, valued at US$ 745 million in 2023, is on a strong growth trajectory and is projected to reach US$ 3.1 billion by 2034. This expansion is fueled by the accelerating adoption of wide‑bandgap semiconductor technology across high‑power applications, notably electric‑vehicle (EV) powertrains, renewable‑energy inverters, and industrial motor‑drive systems. The shift from traditional 6‑inch substrates toward larger 8‑inch wafers is a defining competitive advantage, delivering economies of scale, higher throughput, and improved yield for next‑generation power devices.

SiC wafers are distinguished by their superior thermal conductivity, high breakdown voltage, and intrinsic ability to operate at elevated temperatures without the need for extensive cooling infrastructure. These material characteristics enable power electronics designers to achieve higher efficiency, reduced form factor, and longer lifecycle-attributes that are critical for the rapid electrification of transport, the modernization of power grids, and the expansion of renewable‑energy generation. As manufacturers seek to meet stringent efficiency standards and regulatory mandates, SiC wafers have become an indispensable substrate for high‑performance power modules.

Download FREE Sample Report:

Silicon Carbide (SiC) Wafer (6‑inch, 8‑inch) Market – View in Detailed Research Report

The surge in EV sales, driven by government incentives, stricter emissions legislation, and consumer demand for cleaner mobility, is directly translating into a robust pipeline of SiC power‑device demand. Simultaneously, renewable‑energy installations-particularly solar‑PV inverters and wind‑turbine converters-are scaling up to meet global decarbonization goals, creating a parallel demand curve for high‑efficiency SiC‑based converters. In the industrial arena, motor‑drive systems for factories, data‑center cooling, and rail‑transport are increasingly specifying SiC devices to cut energy consumption and operational costs. Collectively, these macro‑trends build a strong, diversified foundation for the SiC wafer market’s long‑term growth.

The report underscores that the majority of SiC wafer consumption is concentrated in the Asia‑Pacific region, which accounts for roughly three‑quarters of global demand. This geographic concentration is reinforced by the presence of leading foundries, a deep talent pool in semiconductor manufacturing, and substantial public‑private investment in advanced wafer‑fab infrastructure. The United States, Europe, and emerging markets across South America, the Middle East, and Africa are also gaining momentum, each leveraging regional policy levers and industry consortiums to nurture local SiC ecosystems.

COMPETITIVE LANDSCAPE

Key Industry Players

Global SiC Wafer Market Dynamics

The global Silicon Carbide (SiC) Wafer (6‑inch, 8‑inch) market is witnessing robust growth due to the shifting preference for wide bandgap semiconductors in high‑power applications. The market size reached USD 745 million in 2023 and is projected to reach USD 3.1 billion by 2034, driven by the increasing demand from electric vehicles and renewable energy sectors. The transition from 6‑inch to 8‑inch wafer production is a key competitive differentiator, enabling manufacturers to leverage economies of scale and improve yield rates for advanced power devices.

The competitive landscape is characterized by a mix of vertically integrated companies and specialized foundries that focus on crystal growth and substrate quality. While tier‑one automotive OEMs drive adoption, niche players are establishing footholds by optimizing manufacturing processes for specific diameters and power grades.

Silicon Carbide Wafer Market

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

8‑inch Wafers description with qualitative insights only [Pointers preferred in bullets atleast 2‑3]. The industry is witnessing a rapid transition from the established 6‑inch wafer format towards the larger 8‑inch diameter. This strategic shift is primarily driven by the fundamental economic need for improved scalability and reduced manufacturing costs. Moving to larger wafer sizes allows manufacturers to significantly increase the yield per silicon carbide ingot, directly lowering the unit cost of power devices. This economic pressure is forcing leading semiconductor companies to invest heavily in advanced fabrication capabilities to handle the complexity of larger substrates. The adoption of 8‑inch wafers simplifies integration with existing silicon fabrication infrastructure, thereby accelerating the mass production of SiC power electronics and facilitating their broader market penetration. |

| By Application |

|

High‑Power Applications description with qualitative insights only [Pointers preferred in bullets atleast 2‑3]. The market is fundamentally driven by the superior performance of silicon carbide wafers in high‑voltage and high‑frequency electronic environments. Unlike standard silicon, SiC substrates offer significantly higher thermal conductivity, allowing power devices to operate efficiently at elevated temperatures without excessive cooling. This thermal management advantage is crucial for the electrification of transportation, where compact and efficient power conversion systems are paramount. Furthermore, the wide bandgap properties of SiC enable fast switching speeds, which translates into reduced energy losses during power transmission and conversion. Consequently, automotive and industrial sectors are leveraging these material properties to enhance the efficiency, speed, and reliability of their next‑generation electronic systems, creating a robust demand curve for robust SiC substrates. |

| By End User |

|

Automotive OEMs description with qualitative insights only [Pointers preferred in bullets atleast 2‑3]. Automotive Original Equipment Manufacturers represent a critical growth catalyst for the silicon carbide wafer market as the industry pivots towards comprehensive electrification. The demand stems from the necessity to develop lightweight, compact power electronics that can withstand the rigorous demands of high‑power vehicle platforms. By utilizing SiC wafers in the electric powertrain, manufacturers can achieve extended driving ranges and faster acceleration by minimizing energy dissipation during power conversion. This shift is supported by major automakers aiming to meet stringent environmental regulations and consumer expectations for high‑performance electric vehicles. The sustained investment by automotive giants in powertrain technology continues to fuel a steady and predictable uptake of advanced semiconductor substrates capable of meeting these performance benchmarks. |

| By Wafer Diameter |

|

Economies of Scale description with qualitative insights only [Pointers preferred in bullets atleast 2‑3]. The strategic decision to adopt larger wafer diameters is underpinned by the pursuit of economies of scale, which are essential for the widespread commercial viability of SiC technology in the consumer and industrial sectors. As demand grows, the industry is compelled to maximize the number of functional chips produced from a single ingot. A larger wafer diameter not only increases the throughput of manufacturing lines but also enhances the overall yield potential when combined with mature fabrication processes. This scaling strategy reduces the marginal cost per device, making SiC‑based solutions competitive against traditional silicon technologies. Investors and manufacturers alike are focusing their capital expansion efforts on facilities that can support the processing of larger wafers, viewing this transition as a necessary step for long‑term market leadership. |

| By Crystal Orientation |

|

Superior Material Properties description with qualitative insights only [Pointers preferred in bullets atleast 2‑3]. The choice of crystal polytype is a decisive factor in determining the semiconductor characteristics of the final power device, with 4H‑SiC emerging as the undisputed industry standard due to its superior electronic and thermal properties. While 6H‑SiC has historically been available, 4H‑SiC offers a larger bandgap energy and higher breakdown field strength, which are critical for high‑voltage applications. This specific orientation allows for the creation of power devices that can efficiently handle higher power densities and operate reliably across a wide temperature range. Consequently, leading material suppliers are prioritizing the production and development of 4H‑SiC crystals to ensure that the components manufactured meet the rigorous performance standards required for demanding sectors like power grids and electric mobility. |

Regional Analysis: Silicon Carbide (SiC) Wafer (6‑inch, 8‑inch) Market Trends and Business Strategies 2026‑2034

Robust investments in smart‑grid infrastructure and renewable‑energy projects are creating substantial opportunities for SiC wafer manufacturers across the region.

A distinct shift towards 8‑inch wafer fabrication is underway to meet the growing demands of high‑volume automotive and industrial applications.

The proliferation of electric‑mobility ecosystems in emerging markets is driving the integration of SiC devices to enhance vehicle range and charging efficiency.

Key industries are modernizing power conversion systems, utilizing SiC technology for superior efficiency and reliability under high‑voltage conditions.

North America

North America secures a significant position in the Silicon Carbide (6‑inch, 8‑inch) Wafer Market due to advanced R&D infrastructure and a mature adoption of EV technologies. The United States demonstrates a keen interest in utilizing SiC wafers within aerospace and defense applications, capitalizing on the material's resilience in extreme thermal conditions compared to traditional silicon solutions. Additionally, the region's support for grid‑modernization initiatives supports the demand for efficient power‑conversion systems essential for renewable‑energy integration.

Europe

Europe remains a critical growth engine for the Silicon Carbide (6‑inch, 8‑inch) Wafer Market, largely fueled by strict environmental regulations aimed at reducing industrial emissions. The automotive sector in Europe is actively transitioning to SiC‑based powertrains to maximize efficiency and minimize energy loss in electric vehicles. Furthermore, the region's commitment to green‑energy projects, including wind and solar farms, necessitates the use of high‑performance semiconductors to optimize grid stability and energy transmission.

South America

South America presents a developing landscape for the Silicon Carbide wafer sector, characterized by increasing interest in renewable‑energy projects and industrial modernization. Although the market is currently emerging, the potential for SiC integration into regional power grids is high due to the pressing need for efficient voltage control and distribution. Local industries are beginning to recognize the long‑term cost benefits and technical superiority of SiC devices over conventional silicon options.

Middle East & Africa

The Middle East and Africa region are positioning themselves strategically within the Silicon Carbide (6‑inch, 8‑inch) Wafer Market, driven by mega‑projects focused on energy independence and desalination. The adoption of SiC technology here is primarily targeted at enhancing the reliability and lifespan of power‑conversion units operating in harsh environmental and climatic conditions.

Get Full Report Here:

Silicon Carbide (SiC) Wafer (6‑inch, 8‑inch) Market, Trends, Business Strategies 2026‑2034 - View in Detailed Research Report

click here to visit more insightful Reports

https://semiconductorinsight.com/report/global-noncontact-level-sensors-market/embed/

https://semiconductorinsight.com/blog/tag/future-of-the-printed-circuit-board-market-growth/

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us